Business valuation is the strategic process of determining the total net worth of a business. At its core, determining the net worth of an enterprise means calculating its true equity. Equity is simply defined as total assets minus total liabilities. Understanding how to properly value a business is not just an academic exercise; it is a critical skill for business owners, investors, and corporate strategists. There are several major reasons why a comprehensive business valuation might be required. These include planning for mergers and acquisitions, preparing for a takeover bid, transitioning an unquoted private company to a publicly traded entity (going public), selling business shares to new partners, or using company shares as pledged collateral to secure large bank loans. In this comprehensive guide, we will break down the primary methods of business valuation, with a specific focus on mastering the asset-based approach.

Why Business Valuation is Critical for Your Success

Knowing the precise value of your company empowers you to make highly strategic, data-driven decisions. If you are seeking external capital, venture capitalists and angel investors will immediately demand a valuation to determine how much equity they receive for their cash. Furthermore, if you are planning an exit strategy or retirement, an accurate valuation ensures you do not leave millions of dollars on the negotiating table. Valuation is not a simple guessing game; it requires strict adherence to financial frameworks. The process removes emotional attachment from the founder is perspective and replaces it with cold, hard metrics that external markets recognize and trust.

Overview of the Three Main Valuation Approaches

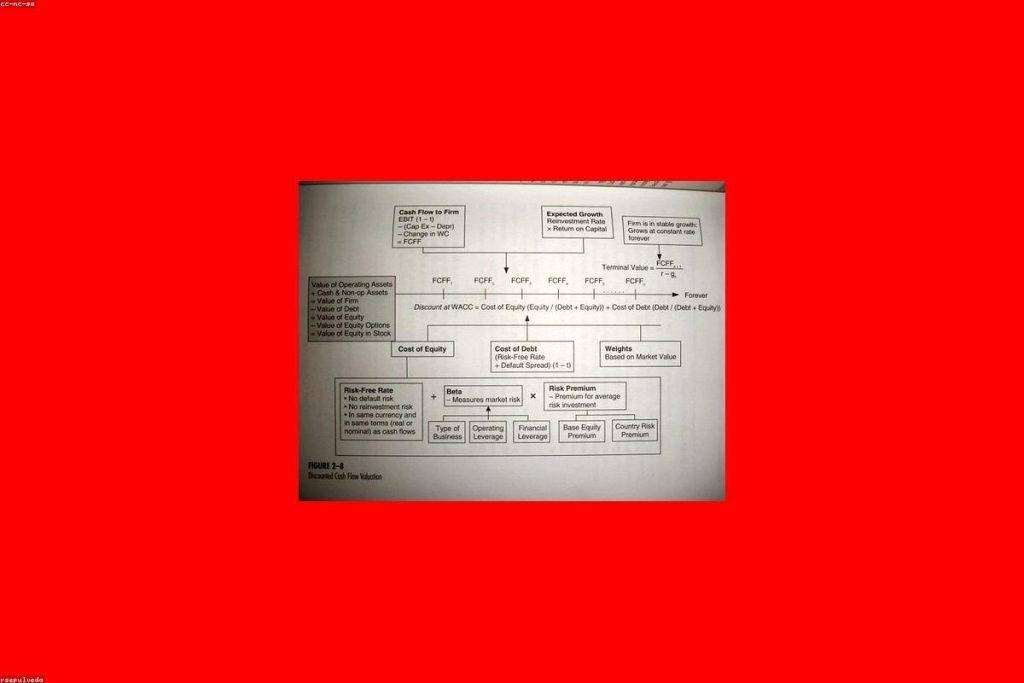

When financial analysts approach business valuation, they typically choose from three primary pillars: Asset-Based, Market-Based, and Cash-Based methods. The Asset-Based Method determines value by analyzing the company is statement of financial position (balance sheet), calculating the worth of tangible assets, and deducting liabilities. The Market-Based Method relies heavily on current market information, utilizing metrics like market capitalization, price-to-earnings (P/E) ratios, and market-to-book ratios. This method is highly effective when efficient, transparent public markets exist to provide comparable data. Finally, the Cash-Based Method revolves around the company is ability to generate liquid wealth in the future. This includes models like the Dividend Valuation Model, Free Cash Flow analysis, Discounted Cash Flow (DCF) techniques, Economic Value Added (EVA), and Adjusted Present Value. Each method serves a specific purpose depending on whether the company is liquidating, expanding, or paying out heavy dividends.

Deep Dive into Asset-Based Valuation Methods

The Asset-Based Method is often considered the most grounded approach because it relies on physical, verifiable items. Under this umbrella, we look at three distinct variations. The first is the Book Value Method. This uses the historic cost of tangible assets exactly as they appear on the balance sheet, minus all liabilities. Intangible assets (like brand reputation) are totally excluded unless they have a strictly defined market value. The second variation is the Replacement Cost Method. In this scenario, we value the assets based on what it would cost to acquire them today in the open market. If a specific asset is replacement price is unavailable, the book value is used as an approximation. The third variation is the Net Realizable Value Method. This asks: what would these assets sell for today? This is heavily utilized when a company is facing liquidation or bankruptcy, as it relies on the immediate market estimate or salvage value of the goods, rather than their ongoing operational value.

Step-by-Step Practical Example of Asset-Based Valuation

To truly understand this, let us walk through a real-world mathematical application using the Net Asset Basis, Replacement Cost, and Realizable Value bases. Imagine a company, ABC PLC. First, we identify all assets. We take the Non-Current Assets (machinery, property) and the Current Assets (inventory, receivables, bank balances). Under the Book Value (Net Asset) Basis, we might have $600k in non-current assets, $500k in inventory, $700k in receivables, and $150k in the bank, totaling $1.95 million. Under the Replacement Cost Basis, these figures might adjust (e.g., non-current assets cost $650k to replace, inventory costs $600k), bringing total assets to $2.1 million. Under the Realizable Value Basis (liquidation), assets are marked down to what they can quickly sell for. Let us say 10% of our $700k receivables are irrecoverable bad debts. We must subtract $70k, leaving $630k in realizable receivables. The total realizable asset pool might drop to $1.53 million.

Leveraging Valuation Data for Strategic Growth

Once you have your total asset figures across the three methods, the next step is universally the same: subtract the liabilities. If ABC PLC owes $550k in trade payables and has a $350k bank overdraft, total liabilities are $900k. Subtracting $900k from our Book Value assets ($1.95M) gives an equity value of $1.05 million. Subtracting it from our Replacement Cost assets ($2.1M) gives $1.2 million. Subtracting it from our Realizable Value ($1.53M) leaves $630k. To find the value per share, we simply divide the total equity by the number of issued ordinary shares (let us say 650,000 shares). This yields a per-share value of $1.62 under book value, $1.85 under replacement cost, and $0.97 under liquidation realizable value. Armed with this robust, multi-tiered data, corporate leaders can confidently approach buyers, negotiate better loan terms, or set highly accurate initial public offering prices. Valuation is the ultimate map for corporate financial strategy.